The Signal for Change

The Signal for Change

“We are running the most dangerous experiment in history right now, which is to see how much carbon dioxide the atmosphere can handle before there is an environmental catastrophe.” Elon Musk

Last week’s proposed rules that may require public companies to produce climate disclosures are but the latest headline in what has been an increased inventory demand for disclosure around climate risks and their material impacts. A risk that has been underpinned by the Task Force on Climate-related Financial Disclosures (TCFD) framework since 2017.

This week, let’s take a look at some of the factors that have led to the latest proposed rules and, more importantly, discuss how to take this into account in your ESG program.

Since I mentioned TCFD already, let’s start with the 2017 release of climate-related disclosure recommendations and their stated goal of supporting informed capital allocation through governance, strategy, risk management, and metrics/targets.

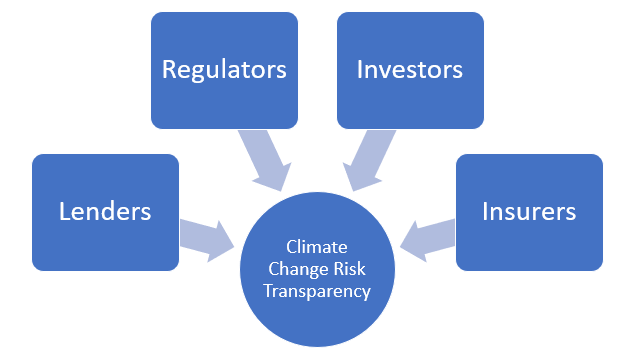

The vision of TCFD, and the reason it resonates with investors, is its position that investors, lenders, and insurers don’t have a clear view of how companies will perform in the face of environmental changes related to the climate. The framework takes into account not only the actual physical risk of direct impact but also the potential impact of changing regulations, new technologies, and customer behavior shifts.

If you would like to take a deeper dive into the TCFD final report of recommendations, a link can be found here.

While we tend to focus on the investors, I want to point out another party here that will be instrumental, the insurers. In the past five years, natural disasters have cost the United States more than $600 billion. As the climate continues to warm those costs are expected to increase as the size and intensity of severe weather events increase. That dynamic actually threatens the insurer’s business model, forcing insurers to reevaluate the risk posed to insured assets due to climate change.

You can think of insurance as a giant pot of money. The insurer pools the risk across its account holders so when a policyholder suffers harm, the money in the pot covers the policyholder. Insurers put a great amount of time and resources into calculating the risk to make sure the pot has enough to cover the risk, and that statistically, only a small number of policyholders are likely to suffer an insured harm in a given period.

This model breaks down when large portions of the insured population suffer harm at the same time, which is often the case with climate-related events. This means to counter this, insurers will either have to raise rates to make sure enough money is in the pot or exit the market entirely due to the risks of that particular market.

According to Blackrock research, insurers are starting to take notice, and 36% of the respondents surveyed named environmental risks as one of their most serious macro risks. The result is an overhaul of insurance distribution models, an increased focus on sustainability, and the application of digital technology in the industry. For a deeper dive on the 2021 Blackrock Global Insurance Report, click here.

Those insurers will be demanding increased risk analysis and transparency into assets that their policyholders desire to put under the coverage plan.

The final area to consider in accessing climate risks are lenders. For lenders, physical risks associated with the changing climate and the associated costs are top of mind for most financial institutions. As a result, lenders have been actively collecting information on the regional climate risks in addition to evaluating property-specific data around resiliency.

While no standard methodology has emerged on how these risk evaluations will be done, in 2021 an ASTM task force was formed to create an ASTM Guide regarding the assessment of climate risk and resilience of commercial buildings. While the task group work continues, we got some insight in February 2022, during an interview with the Task Group Chair.

For those not familiar, ASTM International is one of the largest voluntary standards organizations in the world. When the ASTM provides guidance, it gets a lot of attention. In this case, the vision appears to be an umbrella referencing existing natural hazard and climate change-related resilience frameworks.

The task force seems to be gravitating to a Property Resilience Assessment (PRA) that will consist of three main phases:

Natural Hazard Screening Stage: This identifies those hazards that are likely concerns of the property. This stage leverages publicly available and commercially available hazard maps and models.

Risk Assessment Stage: this document review and site inspection looks specifically at the property attributes including construction materials and age to identify sensitivities and vulnerabilities.

Basic Resilience Measures Stage: here resiliency measures are identified that can help to property withstand a shock or stressor such as flood barriers, the location of critical equipment, etc.

The ASTM Task Force anticipates having a guide out for approval by the end of 2022. Find additional information on the Task Force's progress here.

Not to be forgotten are the regulators, just as I started this article referencing the proposed SEC rules that would require public companies to produce climate disclosures similar to the TCFD framework. This proposed SEC rule is not alone, however, performance ordinances have been passed across the United States, from Colorado and Washington state to New York City, Boston, St. Louis, and the District of Columbia. In the European Union, the Taxonomy Regulation was passed in June of 2020 and went into force in July of the same year. Similarly, in late 2020, the United Kingdom followed suit with its own green taxonomy.

With each day, the pressure on organizations grows to measure the Climate Change risks and disclose those risks. To do this, the risk must be identified and its potential impact revealed to understand the potential impact. Standards need to be leaned on to ensure that the significance and probability of risk are included in the assessment. Risks also pose the potential for mitigation and even capitalizing on the opportunity if the mitigation is effective. Oftentimes, the reward is only a couple of steps away from risk.

You can help reduce the impact of the built environment by sharing this blog with your peers. Together we can impact the 39% of greenhouse gasses attributed to the built environment. It starts with awareness, and we succeed with teamwork.

Stay well!

Chris Laughman is the ThirtyNine Blog author, a blog dedicated to reducing the impact of the built environment. When not blogging, Chris is helping the real estate industry reduce energy and water impact as the Vice President of Sustainability for Conservice, the Utility Experts. Whether Multifamily, Single Family, Student Housing, Commercial, or Military, we simplify utility billing and expense management by doing it for you. Our insight into your utility consumption provides an opportunity to identify risks. Leveraging innovation and experience we ignite solutions with real impacts and track performance to ensure the trendline stays laser-focused on the goal. At Conservice we have developed a true bill-to-boardroom solution to help truly make a difference. We have before us a tremendous opportunity. Standing shoulder to shoulder, we will get this done. Contact me at claughman@conservice.com for more information.

Follow us at:

Twitter: @BlogThirtynine

Instagram: ThirtyNine_Blog