Solar Financing - From PPA's to Tax Credits - What is Your Plan?

When it comes to solar, there are a lot of questions ranging from how it works to how do you pay for it. This week, I wanted to peel back the financial aspects of Solar a bit so we all have a base level. That said, this article is by no means in-depth enough to dive too deeply into the financial mechanisms that can be leveraged. But hopefully, you will be prepared to start to have those conversations. I’d also love to get your feedback as well - what are you doing, and what have you seen? This is definitely an area with a lot of information and misinformation.

At its most basic level, a solar installation will typically consist of three components:

Capital/Equity

Debt

Tax Credits/Incentives

Of course, the simplest way to acquire solar is to purchase it through a capital expenditure. Simply lay out the cash, execute a contract with an installer, coordinate with the installer to get utility authorization if interconnecting to the grid, and then calculate the return on investment. While simple, it may or may not be the best use of capital to simply purchase a system.

Purchases can take many forms, and referring to the three components of a solar deal noted above, unless it is an equity purchase, the impact of the tax credits and the way the debt is structured can be beneficial.

Debt means financing, and the project’s financial structure can take many paths. Solar leases and Power Purchase Agreements (PPAs) are the two most common, and the primary difference is in the payment structure and what the payment is based on.

In the lease model, the customer signs a contract with an installer/developer and pays for the use of a solar system over a specified period of time. This is not really different than leasing a vehicle. The installer/developer will pay for the installation and, typically, the maintenance of said system. In return, the power produced by the system belongs to the entity leasing the solar array. This allows the asset to avoid part or all of the upfront cost of the array.

The lease may provide for some guarantees around the production of energy the system will generate, but the payment structure is really based on a set payment plan over a specific period of time. The lease is no different than any other lease, so it can have credit implications. In terms of ownership, the solar array belongs to the entity leasing the array to the property; thus, any tax credits of RECs would belong to the Developer.

The lease term can be as short as ten years or as long as 30 and typically can be transferred to new ownership if the building is sold during the term. Pay attention to early termination clauses; they may provide alternative resolutions if the purchaser does not want to acquire the solar array with the asset. As the array tends to add value to the asset, it is rare that they are not simply transferred to the new owner - but always good to know your options.

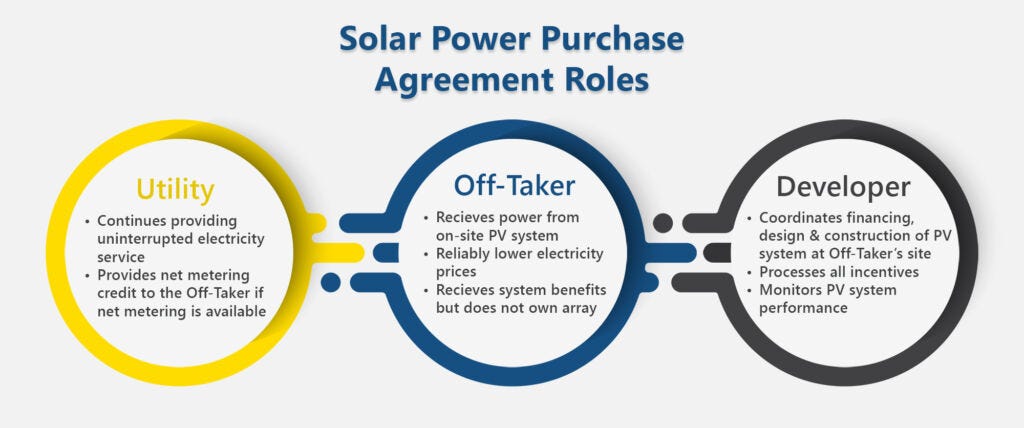

The other vehicle is the PPA, and there are different models of PPA. In general, the PPA, at least at first, looks a lot like a solar lease. The Developer installs and finances the solar array; thus, the property avoids the initial capital outlay. However, instead of a payment plan based on time, the property pays the Developer for the power consumed by the property. This rate is typically lower than the utility rate but would include costs and profits for the PPA developer.

The solar PPA is typically an off-balance sheet financial arrangement. In this arrangement, the energy customer (called the Off-Taker) is the party receiving the power from the property. While this is typically the property the array is installed on, there are arrangements that allow for some variation. For example, the actual array may provide power to the grid, and a separate property picks up the power through an agreement. This is also a PPA; in either case, the entity receiving the power is referred to as the Off-Taker.

The Developer is the entity coordinating the financing, design, and installation of the array. They “own” the array and are responsible for maintenance. As the owner, just like in the lease model, the Developerretains the RECs and any tax credits or other incentives. As the Developer is paid based on the energy delivered, they will monitor the energy delivered and are incentivized to deliver as much energy as possible. Due to this incentive to provide as much energy as possible, it is not as common to see an energy delivery guarantee with a PPA. Similar to the lease, the PPA term can be as short as ten years or as long as 30. It can also be transferred to the new ownership if the building is sold during the term and has provisions for alternative termination arrangements if the new owner doesn’t want the array.

Of course, unless the asset is off-grid, the other party involved is the Utility. There will be requirements, including interconnection procedures and metering specifications. The Developer will typically take the lead on meeting with the local Utility and ensuring all requirements are met in order to get approval for the installation.

The lease or PPA offers a potential hurdle for real estate brokers in that the property title is encumbered. In prior years, this was more of an issue; however, as the solar array benefits the property through lower utility costs and more reliable energy, its presence tends to be viewed as a net positive. In either the lease or PPA, if the property is sold and the new owner does not want the system as part of the acquisition, the system can be removed and the agreement terminated.

Another variation of the PPA is when the actual Off-Taker is not the property but rather the residents of the property. In this variation, the property owner may be paid rent for the use of the roof space, and the Developer is granted exclusive access to sell the energy to the residents directly. State regulations impact how or if this arrangement is viable.

In the case of PPAs and leases, another regulatory factor that can either help or hurt the deal is the state regulations around Virtual Net Metering. One of the more costly components of the solar array is the grid interconnection, and the more interconnections, the more expensive the project. Those states that allow virtual net metering provides a mechanism in which all meters on the property can benefit from the solar, but every meter doesn’t need an independent interconnection. This makes states like California and Colorado very attractive, as you can deliver more energy under the agreement without the added costs of multiple interconnections.

For this to work, a billing mechanism has to be established in which the residents are billed for the combination of grid and solar power provided. This can also provide a bit of a wrinkle, as some utilities do not include enough information on their bill to actually calculate this resident bill. In these cases, a submeter may need to be added to the residential unit in order to calculate the resident’s energy use and allow for bill back for the combined solar and grid energy.

Other state regulations will likely impact what the options are in each state. Take Texas, for example, a complicated state, as each resident has a supplier choice. This means the property owner cannot guarantee full property participation. In this case, the program has to be set up to provide the residents an opportunity to “opt out” so that they can select their own supplier if they choose. To offset the potential loss of some resident supply, the Developer, in those cases, will often have their on-site generation set up to provide supply to the grid instead of supply to the resident who has opted out. This scenario may also offer battery backup, in which demand or time of use can be managed to a higher degree.

The last component of the solar deal is the tax credits and incentives. In 2020 and 2021, solar PV system owners could take a tax credit of 26% of the installation cost. In August 2022, Congress extended the Investment Tax Credit (ITC) and raised it to 30% for systems installed between 2022 and 2032, with tiers reducing the credit to 26% in 2033 and 22% in 2034.

Of particular interest to REITs, the Inflation Reduction Act includes a provision that allows certain taxpayers, including REITs, to elect to transfer the ITC to an unrelated taxpayer in exchange for cash. Included in this provision is a language that specifies that the amount received by the seller is not includible in gross income. In addition, another provision would turn off the ITC Limitation in the case of a REIT that elects to transfer the ITC allowed with respect to a solar facility.

Under the Income Test, if the REIT elects to transfer the ITC allowed with respect to a solar facility, the amounts realized would not be considered for purposes of the Income Test. In cases where the REIT consumes the electricity generated by the solar facility, and assuming there is no income from the sale of the environmental attributes such as Renewable Energy Credits (RECs), the REIT would not have any income from the solar facility itself. This is a significant change as the Income Test, which requires at least 75% of the REIT’s gross income for each taxable year to be derived from real estate sources, and that at least 95% of the REIT’s gross income for a taxable year be derived from such real estate sources and certain types of passive income, led to REITs owning solar through taxable REIT subsidiaries (TRS), which have their own challenges. While you need to review this with your own REIT and tax experts, this limitation seems to be addressed under the Inflation Reduction Act (source).

Even when trying to outline solar in a simplified format, it can get complicated quickly. What is clear is there is no uniform solar strategy that you can apply across your portfolio. Every site will be different - different utility rules, financing options, energy generation capabilities, etc. While you can coordinate a strategy with a common developer, that strategy will be nuanced at the state and asset levels.

While it may take a bit more work, and a more complicated strategy, an effective solar strategy can reduce operational expenses, provide more reliable energy to the site and potentially even generate revenue.

You can help reduce the impact of the built environment by sharing this blog with your peers. Together we can impact the 39% of greenhouse gasses attributed to the built environment. It starts with awareness, and we succeed with teamwork.

Stay well!

Chris Laughman is the ThirtyNine Blog author, a blog dedicated to reducing the built environment’s impact. When not blogging, Chris is helping residents, clients, and investors reduce their energy, carbon, waste, and water impact as the Senior Director of Energy and Sustainability for Greystar. Our team’s insight into the utility consumption of our managed and owned portfolios provides insight into opportunities to identify and mitigate risk. We leverage innovation and experience to ignite solutions with real impacts while tracking performance, ensuring the trendline stays laser-focused on the goal. We in real estate have a tremendous opportunity to make a difference in the built environment. Standing shoulder to shoulder, we will get this done. I can be contacted at: chris.laughman@greystar.com for questions, concerns, or collaboration.

The opinions expressed in this blog are my own.

Follow us at:

Twitter: @BlogThirtynine

Instagram: ThirtyNine_Blog