ESG Update

The first rule of any technology used in business is automation applied to an efficient operation will magnify efficiency, (but) applied to inefficiency will magnify inefficiency...Bill Gates

From time to time, it is good to step back and take a look at our industry, the trends, and the implications for ESG. Recently, Real Page released their quarterly apartment demand study, which provides some interesting insights and potential implications for ESG. What is striking is in this most recent report, we see negative apartment absorption in the third quarter, a quarter that for the past 30 years has delivered positive absorption. According to Jay Parsons and Carl Whitaker in their latest Real Page market review, we seem to be experiencing a freeze in household formation. While the earlier quarters this year delivered strong absorption results, this latest quarter, when considered with the normally lower 4th quarter, may flatten out the results from earlier in the year.

We also saw vacancy slide a bit, although it has been at historic highs, and the 95% rate it stopped at is still very strong. Meanwhile, in the economy, we see wages and employment remain high. This explains why the impact is at all levels of housing equally and in nearly all markets. It is not a factor of consumers not being capable of absorbing the continued increase in rates. Instead, it seems to be signaling market uncertainty; wages are going up, and unemployment is remaining low, yet consumers just are not sure. They are not wanting to increase their housing costs (source).

What it does mean for the market is until that uncertainty is resolved, we cannot continue to successful push up rental rates. As an ESG professional, why is this important? When we think about rental housing, the industry’s go-to lever for the past decade has been increasing rent in order to increase net operating income (NOI). So what happens when you cannot increase the rent but need to increase NOI?

When you stop and think about it, reducing expenses by $1 has the same effect on NOI as raising rent by $1. This may indicate that now is a good time to find operational efficiencies.

So what are investors are thinking? After all, for investors, real estate is often seen as an inflation hedge. A recent PWC study shows ESG-related assets under management (AUM) continue to surge and are tracking to reach $34 trillion (21.5% of all assets) by 2026 (source). This study was accompanied by another study by KPMG, which surveyed CEOs and provided a similarly positive outlook. With 85% of CEOs feeling confident in their companies’ growth prospects and resilience (source).

Another investor indicator is the annual GRESB results, publicly released yesterday. While those that participate in GRESB tend to be ESG leaders and emerging leaders, this past year’s results revealed another increase in participation at 20% and now represent 1,820 entities with a combined 6.9 Trillion in assets benchmarked - 150,000 total individual assets. Much of that growth is in the Americas, which added 111 additional portfolios and represents nearly 3 Trillion in assets (source). There is a reason why GRESB participation continues to increase - because investors are demanding it.

So investors and CEOs remain enthusiastic, and their investments provide evidence that this isn’t just marketing. What about the government? The Department of Labor helped underscore additional confidence in the importance of ESG with their recently proposed rule on Labor ESG investment and proxy voting. This rule acknowledges that “ESG factors may be material to the risk-return analysis of a portfolio and that a fiduciary’s analysis may often require an evaluation of the economic effects of climate change and other ESG factors” (source). Certainly, this rule provides a loud response to those states who jeopardized their pension investments by prohibiting the consideration of these factors in returns. This position was further emphasized by Morningstar in their recent study, which revealed that 85% of respondents took the position that ESG factors are “very material” or “fairly material” to the investment process (source).

Finally, the insurance industry again signaled that organizations that are not environmentally conscious pose a higher risk to insure and may risk either paying higher premiums or losing coverage entirely. This time the signal was Munich Re, the world’s largest reinsurer, who ended support for coverage on new oil and gas fields, now oil infrastructure, and new oil plants (source). This position was accompanied y another study in Adaption Leader, which forecasts the insurance industry pulling away from coverage of fossil fuel-based infrastructure due to risks posed by energy transition risk and higher premiums for those organizations that fail to include adaptation and resilience strategies in their asset assessment (source).

The evidence seems pretty clear; the importance of ESG is going nowhere. Further, if anything, with the current economic trends, it is increasing in importance. Not only to gain access to capital and mitigate risk but also as a strategy to improve NOI as rent increases look to potentially cool.

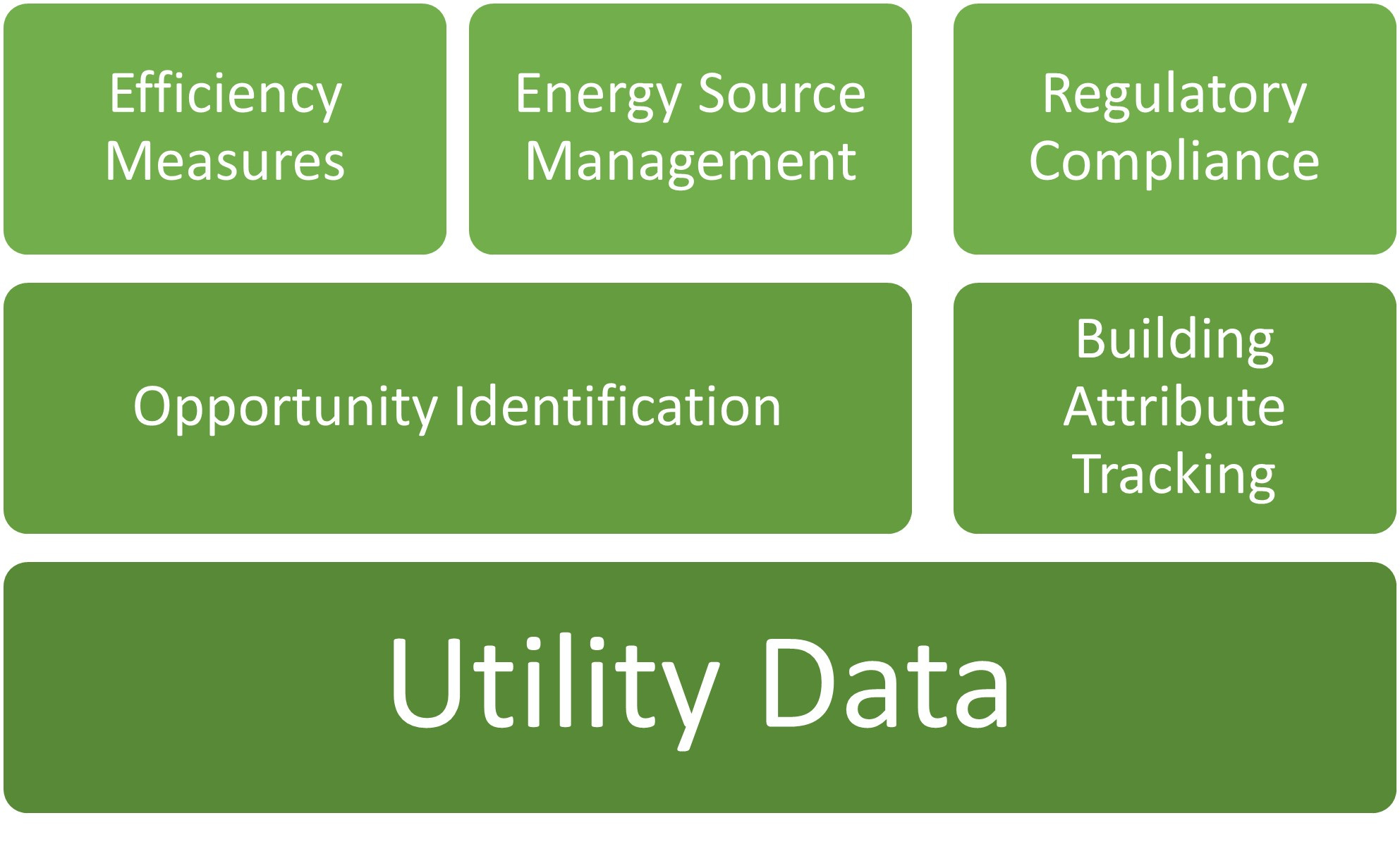

So what should we be doing? We need to be doubling down on our data collection and analysis. Understanding where opportunities are to reduce consumption can have far-reaching consequences; however, taking actions where there is reduced opportunity likely weakens your impact.

We need to be evaluating our energy generation. The combination of flat rent increases and US residential electrical rates increasing an average of 8% in 2022 forecasts a negative NOI impact without taking action. Not only should this action include efficiency, it should also include getting smarter about procurement and on-site electrical generation.

This time-tested strategy provides your assets with the best opportunity to maximize NOI, even if rents cannot be raised. It provides the opportunity to align with investor or organizational goals and comply with local performance reduction laws. It provides a path to reduce insurance premiums and provides the residents with an experience that leaves them feeling that their health and well-being are important.

You can help reduce the impact of the built environment by sharing this blog with your peers. Together we can impact the 39% of greenhouse gasses attributed to the built environment. It starts with awareness, and we succeed with teamwork.

Stay well!

Chris Laughman is the ThirtyNine Blog author, a blog dedicated to reducing the built environment’s impact. When not blogging, Chris is helping residents, clients, and investors reduce their energy, carbon, waste, and water impact as the Senior Director of Energy and Sustainability for Greystar. Our team’s insight into the utility consumption of our managed and owned portfolios provides insight into opportunities to identify and mitigate risk. We leverage innovation and experience to ignite solutions with real impacts while tracking performance, ensuring the trendline stays laser-focused on the goal. All of us in real estate have a tremendous opportunity to make a difference in the built environment. Standing shoulder to shoulder, we will get this done. I can be contacted at: chris.laughman@greystar.com for questions, concerns, or collaboration.

The opinions expressed in this blog are my own.

Follow us at:

Twitter: @BlogThirtynine

Instagram: ThirtyNine_Blog