Engaging Stakeholders through Messaging Strategy

Engaging Stakeholders through Messaging Strategy

An Annual Corporate Sustainability Report when effectively produced can reinforce stakeholder alignment and highlight organization commitment

To some, the Corporate Sustainability Report is a crowning achievement, a carefully crafted communication tool to relay to stakeholders elements of your ESG program that you want to make sure they know about. However, while the report can be a powerful tool, it can also be ineffective when the data presented is not relevant. Often we see companies making proclamations of net-zero or other seemingly important commitments - but important to who?

The first step in developing an ESG Strategy is to understand why you are creating a strategy. What are you trying to address? Does the plan meet the expectations of clients, investors, employees, or other stakeholders?

Similarly, when developing your Corporate Sustainability Report, you need to consider what message you want to relay to your stakeholders. This may include determining what frameworks and metrics are relevant and using the report and these metrics to demonstrate the organization’s commitment to meeting stakeholder expectations.

One framework to keep an eye on is the ISSB or International Sustainability Standards Board. While we can point to many studies that connect ESG performance and corporate financial performance, this increased attention on ESG reporting has led to multiple frameworks being presented, including:

CDP – Carbon Disclosure Project

CDSB – Climate Disclosure Standards Board

GRI – Global Reporting Initiative

IIRC – International Integrated Reporting Council

SASB – Sustainability Accounting Standards Board

TCFD – Taskforce on Climate-Related Disclosures

WEF IBC – World Economic Forum International Business Council

Each of these frameworks is backed by reputable organizations and tend to be voluntary, although there has been some movement to require reporting, such as the New Zealand 2021 law, which mandated TCFD reporting. However, the sheer number and the differences in reporting criteria have left some organizations questioning what they should focus on. This confusion led to demands for consolidation of the various frameworks, and in 2021 the ISSB stepped in to meet these demands for a more consistent approach.

In March of 2022, the first two ISSB standards were released in draft form for input:

IFRS S1– General Requirements for Disclosure of Sustainability-related Financial Information (the General Requirements Standard)

IFRS S2– Climate-related Disclosures (the Climate Standard)

Of particular importance in regards to what information needs to be included in a Corporate Sustainability Report (CSR), IFRS S1 lays out a standard intended to encourage companies to disclose ESG information accurate and relevant enough to provide a good window into their risks and long-term health, and help investors make informed decisions regarding the company. When considering if your CSR meets the expectations of your stakeholders, IFRS S1 provides a solid starting point of transparency and disclosure.

IFRS S2, meanwhile, seems to align with the SEC proposed rule on climate-related disclosures and EU and UK taxonomy measures aimed at the disclosure of information about the organization’s exposure to significant climate-related risks and opportunities.

The public comment period for both drafts closed July 29, 2022, so we expect the ISSB to take that feedback and finalize these drafts, with an anticipated final release by the end of 2022.

In addition to frameworks, the organization also needs to consider the sustainability ratings to be included. Similar to frameworks, the ratings that may be leaned on vary greatly and provides an independently determined, standardized indicator of the organization’s sustainability performance based on a specific set of criteria. These ratings are usually solicited and paid for by the entity being rated and include:

GRESB - Global Real Estate Sustainability Benchmark

Sustainalytics

S&P Global Corporate Sustainability Assessment

Science-Based Target Initiative

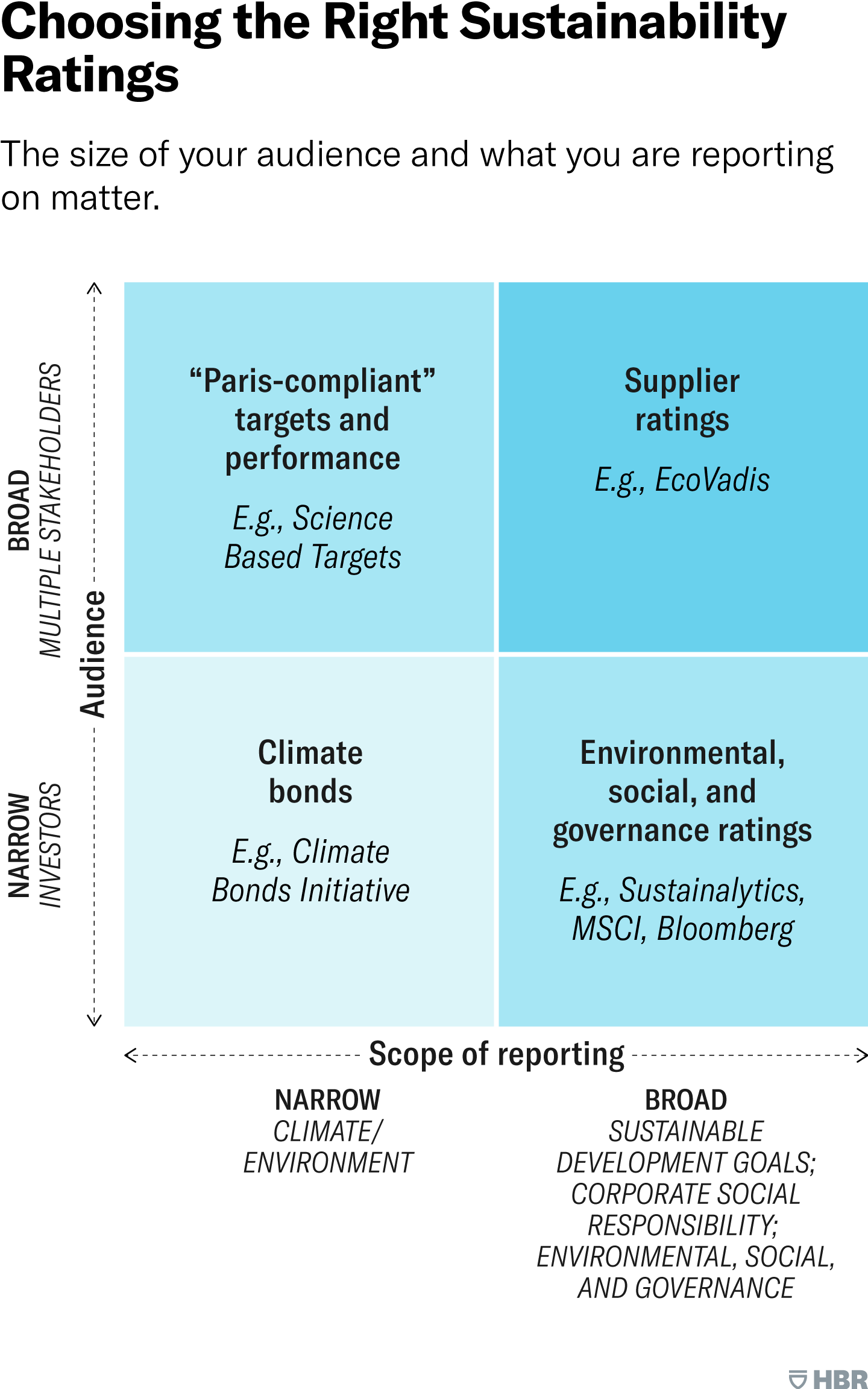

The Harvard Business Review provided the following matrix to help evaluate sustainability ratings:

In order to meet the data requirements of these standards requires, the organization to identify and collect the data called for under each reporting standard. This data may include utility data such as energy and water use, greenhouse gas data, or supply chain questionnaires. This underscores the importance of the second step in ESG strategy, collecting data. In fact, in a 2019 ESG Global Survey published by BNP Paribas, 66% of asset owners and asset managers cited data and reporting issues as the most significant barrier to greater adoption of ESG across their portfolios.

Another consideration is the inclusion of the Global Reporting Initiative (GRI) Framework in the development of the CSR. While not an absolute requirement, particularly for your initial CSR, following the GRI framework increases company accountability and provides transparency surrounding sustainability goals, efforts, and outcomes. The GRI reporting framework consists of universal standards and topic standards that organizations can use to prepare and report information that showcases significant sustainability impacts.

GRI reporting is broken down into a five-step process:

Step 1: Prepare - Organizations define a vision for the report, create a report team, develop a plan of action, and set a kickoff meeting.

Step 2: Connect - Companies identify, hold meetings, and set priorities with key stakeholders in order to determine reporting priorities and define scope.

Step 3: Define - The reporting team selects issues for action and reporting as well as decides on the report content.

Step 4: Monitor - The reporting team monitors activities and records data, checks processes and systems, ensures the quality of information, and follows up as needed.

Step 5: Report - Companies choose the best way to communicate, write, finalize, and launch the report publicly.

GRI also offers various services, tools, and training to guide report teams through different stages of the reporting process, including their materiality assessment.

While the framework, standard, and inclusion of the GRI format are important elements for consideration for CSR inclusion, we must also account for the messaging or theme of the CSR. As noted, the CSR can be a powerful communication tool and can be part of an effective marketing strategy to ensure your ESG message is being relayed to stakeholders.

One of the most potent tactics in reinforcing this messaging is the inclusion of case studies. These stories can help the reader connect the program’s effectiveness to concrete examples, making it easier to visualize the impact. Often these stories can be opportunities to document progress towards goals and highlight the organization’s progress.

It should be noted that the inclusion of stories can also negatively impact the CSR report. This tends to happen when the stories overwhelm the messaging or the overall CSR includes so many messages that the program’s overall effectiveness becomes lost in the CSR report. For this reason, the materiality of the report to the stakeholder must be foremost in mind during report creation. I would recommend no more than 20 significant issues be identified in any individual CSR. You are looking for topics that genuinely “move the needle,” not that “muddy the message.”

As the CSR strategy begins to form, keep in mind the importance that your sustainability story aligns with your company’s business strategy, ambition, and culture. This messaging is essential to demonstrate how organizational business decisions, operations, risk management, and product development/innovation align with the ESG strategy and together are critical to the company achieving its mission.

Your CSR report should be the crowning achievement of your ESG program. With some planning and strategy, it can be a favorable reinforcement of your sustainability message and the organization’s overall commitment.

You can help reduce the impact of the built environment by sharing this blog with your peers. Together we can impact the 39% of greenhouse gasses attributed to the built environment. It starts with awareness, and we succeed with teamwork.

Stay well!

Chris Laughman is the ThirtyNine Blog author, a blog dedicated to reducing the impact of the built environment. When not blogging, Chris is helping the real estate industry reduce energy and water impact as the Vice President of Sustainability for Conservice, the Utility Experts. Whether Multifamily, Single Family, Student Housing, Commercial, or Military, we simplify utility billing and expense management by doing it for you. Our insight into your utility consumption provides an opportunity to identify risks. Leveraging innovation and experience, we ignite solutions with real impacts and track performance to ensure the trendline stays laser-focused on the goal. At Conservice, we have developed a true bill-to-boardroom solution to help truly make a difference. We have before us a tremendous opportunity. Standing shoulder to shoulder, we will get this done. Contact me at claughman@conservice.com for more information.

Follow us at:

Twitter: @BlogThirtynine

Instagram: ThirtyNine_Blog